The Radoff-JEC Group Issues Letter to Fellow Seer, Inc. Stockholders Correcting the Company's Blatant Rewriting of History

Emphasizes that the Radoff-JEC Group Nominees Possess the Necessary Independence and Transaction Experience to Conduct an Objective Review of Strategic Alternatives to Benefit ALL Stockholders

Reiterates the Need for Stockholders to Elect Truly Independent and Qualified Directors to Evaluate Chairman and CEO

This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20260708418902/en/

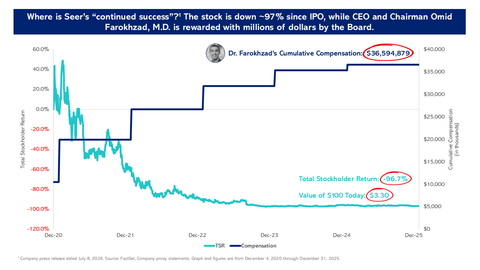

Where is Seer’s “continued success”? The stock is down ~97% since IPO, while CEO and Chairman

***

Fellow Stockholders,

There is a real mismatch between what Seer is now saying and how its management and Board have historically acted. The Company is claiming that Seer has been a “success” and that the directors we are seeking to remove are “critical to Seer’s future.”1 But stockholders like us know the truth:

-

Seer has delivered a -97.0% total stockholder return since going public in

December 2020 .2 -

Seer has generated cumulative reported losses of more than

$465 million since its IPO and virtually zero revenue growth since 2022.3 -

Seer has burned an average of

$51.8 million each year since going public, for a total cash burn of$310.8 million .4 -

Chairman and CEO

Omid Farokhzad , M.D.’s strategic plan – which was presented to the Board – states that Seer will not achieve profitability until 2031, which would be 11 years after the Company went public.5 -

Dr. Farokhzad has sold over$103 million worth of Seer shares since the IPO – more than the Company’s current market capitalization.6 -

The Board rewarded

Dr. Farokhzad with more than$6 million in average annual pay from 2020 through 2025 – more than half of Seer’s average revenue over the same period, totaling~$36.5 million in reported compensation.7 -

Despite Seer’s claim that only two of its seven directors are NOT independent (

Dr. Farokhzad andRobert Langer , Sc.D.), in reality, we contend that FIVE of the directors are NOT truly independent.Terrance McGuire andDipchand Nishar have external business relationships withDr. Farokhzad . Isaac Ro’s employer is a significant investor in Seer’s controlled company PrognomiQ (where he also serves as a director), so his interests and motivations are not aligned with those of Seer stockholders. These issues, and the actions these directors have exhibited to date, raise serious doubts as to their ability to independently and effectively overseeDr. Farokhzad or objectively evaluate his proposal to acquire Seer.8

Seer’s Board Cannot Be Trusted to Evaluate Chairman and CEO Farokhzad’s Acquisition Proposal

The Board’s misleading statements over the past several months have underscored that it is NOT focused on acting in the best interests of ALL stockholders – but only on doing what’s best for itself and

|

Seer’s Egregiously False Claims9 |

The Facts |

|

“Seer has a purpose-built Board of Directors with the expertise needed to guide a category-creating life sciences tools company.” |

Seer’s seven-member Board contains

Directors McGuire and Nishar served on the board of Dr. Farokhzad’s SPAC, which combined with

Is the “purpose” of Seer’s Board to be beholden to

|

|

“Their only desire is to strip Seer of its cash.” |

We never proposed stripping Seer of its cash. Our three acquisition proposals valued Seer appropriately – it is a microcap business that has consistently burned cash and has underwhelming growth prospects.

The cash component of Dr. Farokhzad’s own proposal to acquire Seer is identical to our last offer; yet he does not purport to desire to “strip Seer of its cash.” The Board rejected each of our proposals without engaging with us whatsoever but is now apparently evaluating Dr. Farokhzad’s offer, which we calculate as inferior.

|

|

“[T]heir nominees raise serious concerns regarding independence and their ability to act in the best interests of all stockholders.” |

Our nominees are independent from us and have no relationships that would impact their ability to act in the best interests of all stockholders.

Seer’s Board has failed time and again to act in the best interests of all stockholders, whether by failing to engage with us on any of our three acquisition proposals, seeking to preserve Dr. Farokhzad’s super-voting rights or adopting an onerous poison pill. How can stockholders trust that

|

|

“Three nominees, one purpose: Sell Seer early.”12 |

The purpose of our nominees, as we have consistently said, is to act in the best interests of all Seer stockholders, including by advocating for a strategic review process that focuses on ways to maximize stockholder value after years of destruction. As

|

Vote FOR Independent Directors to Support an Objective Strategic Review

We agree with

The Board chose to reject all three of these offers outright without engaging with us on ANY of them. Then,

We are not opposed to someone who is not us buying Seer. We simply believe Seer should be sold to the highest bidder in a transaction that maximizes value for ALL stockholders – not in a conflict-ridden process led by directors who are chummy with one of the bidders and have demonstrated over the past five-plus years that they cannot create value for Seer stockholders.

Voting for

Sincerely,

Owners of ~7.7% of Seer’s Outstanding Common Stock

***

Vote FOR the Radoff-JEC Group’s Nominees –

Do NOT Vote for

Questions about how to vote? Contact (888) 368-0379 or info@saratogaproxy.com.

Visit www.SaratogaProxy.com/SEER to learn more.

|

1 Company press release dated |

|

|

2 FactSet. Total stockholder return from |

|

|

3 Company Form 10-K for the year ended |

|

|

4 Company Form 10-K filings. Cash burned in operations refers to the sum of net cash used in operating activities, purchases of property and equipment, and proceeds from disposal of property and equipment. |

|

|

5 Company PRE 14A filed on |

|

|

6 Dr. Farokhzad’s Form 4 filings. Market capitalization as of close on |

|

|

7 Company proxy statements. |

|

|

8 Company proxy statements. Complaint filed by |

|

|

9 Company press release dated |

|

|

10 FactSet. Share price decline from |

|

|

11 FactSet. Total stockholder return from |

|

|

12 Company presentation filed on |

|

|

13 Letter from |

|

|

14 Company presentation filed on |

|

View source version on businesswire.com: https://www.businesswire.com/news/home/20260708418902/en/

greg@fondrenlp.com

or

info@saratogaproxy.com

Source: On Behalf of